Are You Ready to Open Your Child’s First Savings Account?

You’ve been talking to your child about money, hoping to start them on the path to a secure financial future. Are you ready to let them begin ...

2 min read

Talking to your kids about finances is an ongoing conversation. Starting with saving coins in a piggy bank and earning an allowance to opening up a savings or checking account, budgeting for major purchases and investing for the future, there are many facets to your child’s financial education. Here is a closer look at teaching your child how to use checks:

Talking to your kids about finances is an ongoing conversation. Starting with saving coins in a piggy bank and earning an allowance to opening up a savings or checking account, budgeting for major purchases and investing for the future, there are many facets to your child’s financial education. Here is a closer look at teaching your child how to use checks:

The basics of checks

It may seem as if checks no longer have a place in modern money management. However, checks serve a vital purpose, and teaching your kids to understand checks represent real money is the first lesson.

Checks provide a record of what money is spent and what’s deposited into their account. A check serves as a receipt, and unlike cash, it has some built-in protections in case it gets lost or stolen. Most places take checks as payment, and as long as there is money in their account, they have “cash” on hand — no need to seek out and stop at an ATM to withdraw money. Checking accounts vary and depending on the account you choose, your teen may be subject to overdraft fees, other fees, and a required balance.

A checking account typically doesn’t have strict limits for the number of deposits and withdrawals, like investment and savings accounts, according to Jake Frankenfield, writer for Investopedia.com. Since checking accounts offer easier access to funds, interest rates tend to be significantly lower or even nonexistent compared to other types of savings accounts, he adds.

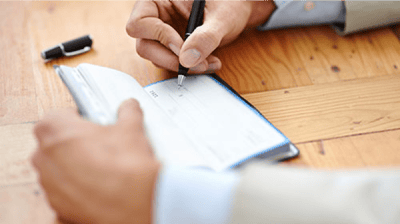

Writing a check

There are five sections your teen must complete to successfully write a check — the date, who the check is going to or recipient’s name, the amount of the check in numerical form, the amount of the check written in words, and the signature line. The memo line located in the bottom left of the check can be left blank, but it can also be the spot where you note additional details about the check, according to Allison Martin of Investopedia.com.

Reading and comprehending a check

A check displays separate sequences of numbers. “The first sequence of numbers represents your financial institution’s routing transit number. This code identifies your bank, allowing the check to be directed to the right place for processing,” adds Martin.

Next to the routing transit number is the checking account number, which represents your teen’s account. The check number is the final set of numbers. This number is visible on the top right of the check, often printed above the date field.

Depositing a check

When your teen receives a check, depositing that money into their account is simple. They will need to flip over the check and sign their name as it appears on the front of the check in the designated endorsement section. Justin Pritchard of TheBalance.com recommends waiting until your teen is at the financial institution or in the process of making the mobile deposit before signing.

Tracking checks and balancing the account

The check register provides a simple way to track the checks your teen writes and deposits. By recording the check number, amount, and the recipient, your teen can review their spending habits. To balance their checkbook, though, your teen will need to compare their register to the statement from their financial institution. They will want to make sure both records match, are free from mathematical mistakes, and factor in any interest, advises Jean Folger on Investopedia.com.

With your help, you can teach your teen how to save, spend, and plan their finances responsibly.

You’ve been talking to your child about money, hoping to start them on the path to a secure financial future. Are you ready to let them begin ...

How to handle money is an important life lesson. The sooner you start your child’s financial education, the more knowledgeable and responsible they...

Strong financial skills are learned. Which is why as parents, it is essential to begin teaching your children about money from an early age. It...