2 min read

How Does a Joint Mortgage Work?

If you can’t afford a house on your own, or if you wish to purchase one together with a friend, a family member, or a partner, a joint mortgage could...

1 min read

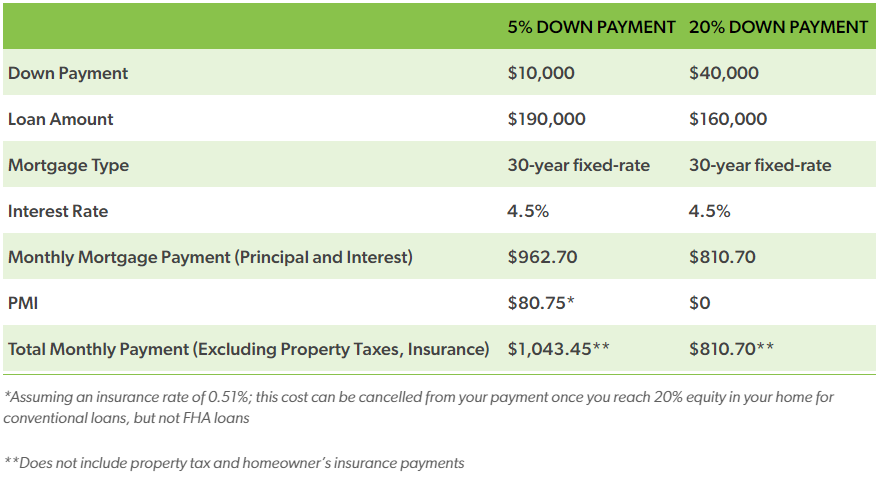

For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

Private Mortgage Insurance (PMI) is typically required on conventional mortgage loans when the borrower's down payment is less than 20% of the home's purchase price. This means that any conventional loan with a down payment of less than 20% will usually require PMI.

Government-backed loans, such as FHA loans and VA loans, have their own mortgage insurance requirements. FHA loans require an upfront Mortgage Insurance Premium (MIP) as well as an annual MIP, while VA loans have a funding fee but do not require ongoing mortgage insurance.

It is not the same thing as homeowner's insurance. It's a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. While PMI is an initial added cost, it enables you to buy now and begin building equity versus waiting five to 10 years to build enough savings for a 20% down payment.

While the amount you pay for PMI can vary, you can expect to pay approximately between $30 and $70 per month for every $100,000 borrowed.

A $200,000 HOME: 5% DOWN VS. 20% DOWN

Once you've built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment. If you're current on your mortgage payments, PMI will automatically terminate on the date when your principal balance is scheduled to reach 78% of the original appraised value of your home. If you choose to use PMI, be sure to talk with your lender about these specific details of your policy.

Talk with First Federal Loan Officer about what down payment makes the most sense for your financial situation. Remember, you have options!

2 min read

If you can’t afford a house on your own, or if you wish to purchase one together with a friend, a family member, or a partner, a joint mortgage could...

As the tax season approaches, many Americans eagerly anticipate receiving their tax refunds. For homeowners, a tax refund can be an excellent...