Homeowners Gained $28K in Equity over the Past Year

If you own a home, your net worth has probably gone up a lot over the past year. Home prices have been rising, which means you're building equity...

1 min read

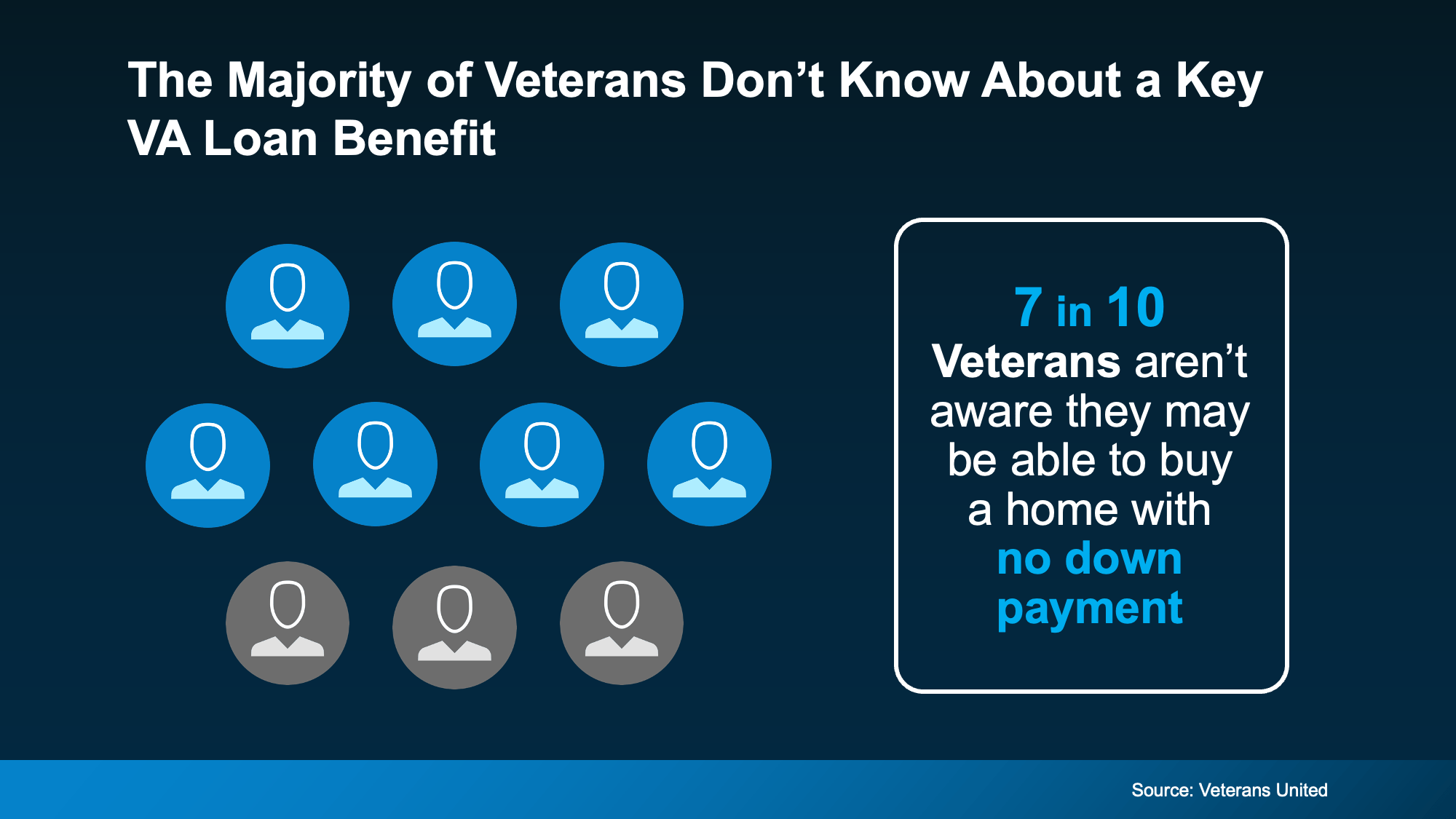

If you’ve served in the military (or if your spouse has), you have access to one of the key home financing options available to eligible service members and veterans. The chance to buy a home with the possibility of no down payment.

Unfortunately, many Veterans don’t know about this benefit, according to Veterans United.

And that’s a big missed opportunity for those who’ve earned this benefit through service. So, let’s break down what you may need to know about Veterans Affairs (VA) home loans.

For nearly 80 years, VA loans have made homeownership possible for millions of Veterans and active-duty service members. Here are just a few of the top perks according to the Department of Veteran Affairs:

These features make VA loans a great way for service members (or their family) to pursue homeownership and potentially reduce certain upfront costs.

Why Your Choice of Lender Matters

The VA loan process can feel complex, especially for borrowers unfamiliar with its unique requirements. That’s why partnering with a lender experienced in VA transactions can be a game-changer. As VA News notes, having a “military-friendly broker who understands the VA home loan application process may help simplify the homebuying experience.”

If you’re interested in tools, resources, or training to better serve your military clients, we’re here to support you.

Connect with a First Federal Bank Loan Officer to discuss how to help you unlock this powerful benefit today.

If you own a home, your net worth has probably gone up a lot over the past year. Home prices have been rising, which means you're building equity...

Did you know? According to a recent study, 72% of people with student loans think their debt will delay their ability to buy a home. Maybe you’re one...

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising...