Do You Know How Much Your House Is Really Worth?

Want to know something important that most people rarely get professionally checked? Spoiler alert: it may be the value of your home.

3 min read

Inflation is moving in the wrong direction again. But before the headlines cause concern, here’s what’s happening, why it matters for the housing market, and what it could mean if you’re thinking about buying or selling.

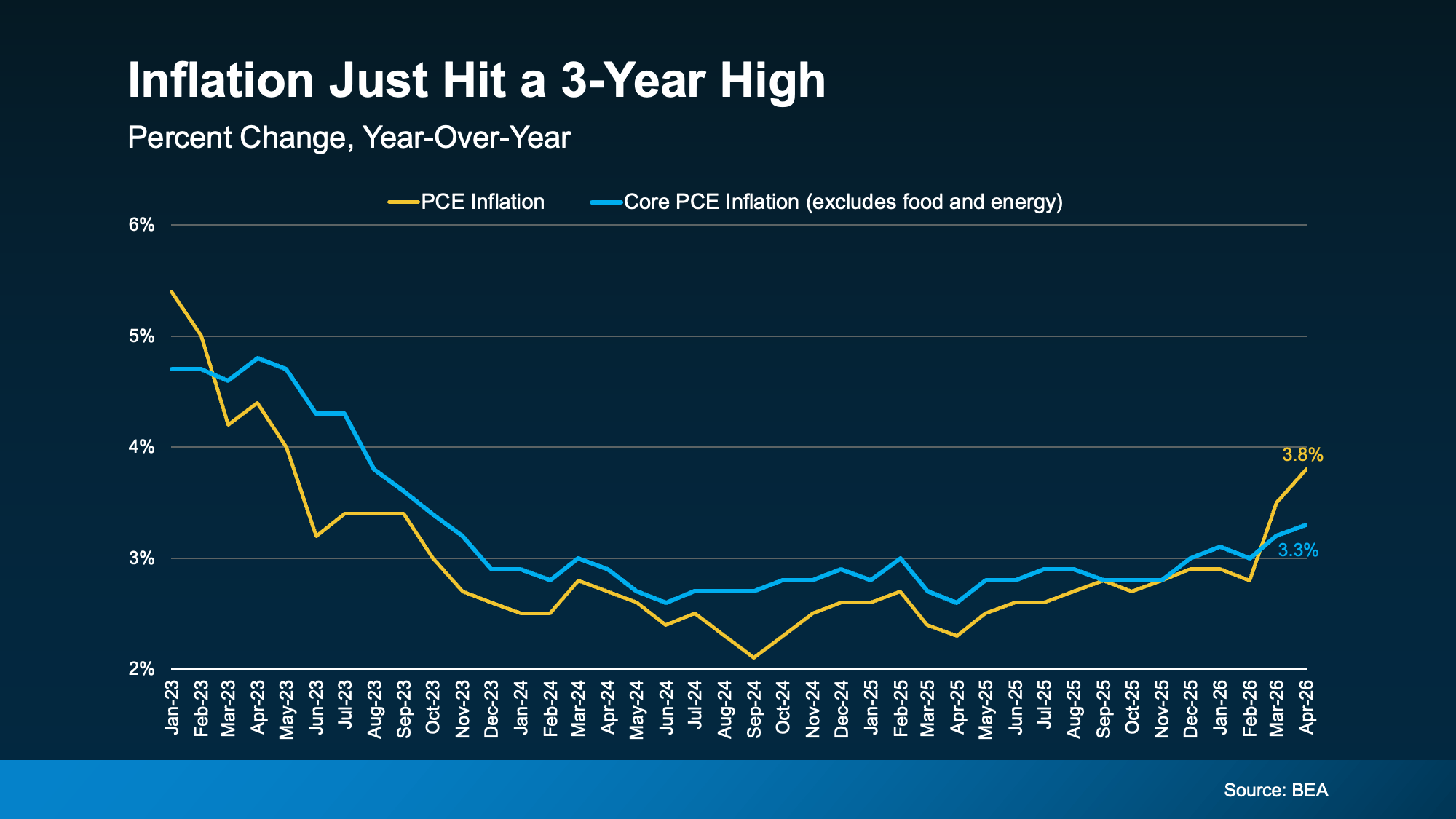

The government tracks inflation in a variety of ways. One is something called PCE – the Personal Consumption Expenditures Price Index. It measures how much more (or less) people are paying for goods and services compared to a year ago. And just based on your own expenses, you can probably guess which way that’s trending.

That’s the number getting attention right now. The yellow line shows how overall PCE has increased since February (see graph below). One major factor behind the recent jump is the ongoing conflict in the Middle East, which has contributed to higher gas and energy prices.

Source: U.S. Bureau of Economic Analysis (BEA), Price Chains and the Origins of PCE Price Growth, April 2026. Historical performance is not indicative of future results.

You may also notice a second line. The blue line shows core PCE. That’s the same inflation measure, but with food and energy prices removed. The Federal Reserve, or the Fed, tends to watch core PCE closely because energy prices can move quickly and may distort the broader picture.

Here’s the somewhat encouraging part: core PCE is rising, but not nearly as quickly as the overall number. That suggests a meaningful part of the recent inflation spike is tied to energy costs and global events. If those pressures ease, inflation trends may improve over time.

Why This Matters for Mortgage Rates

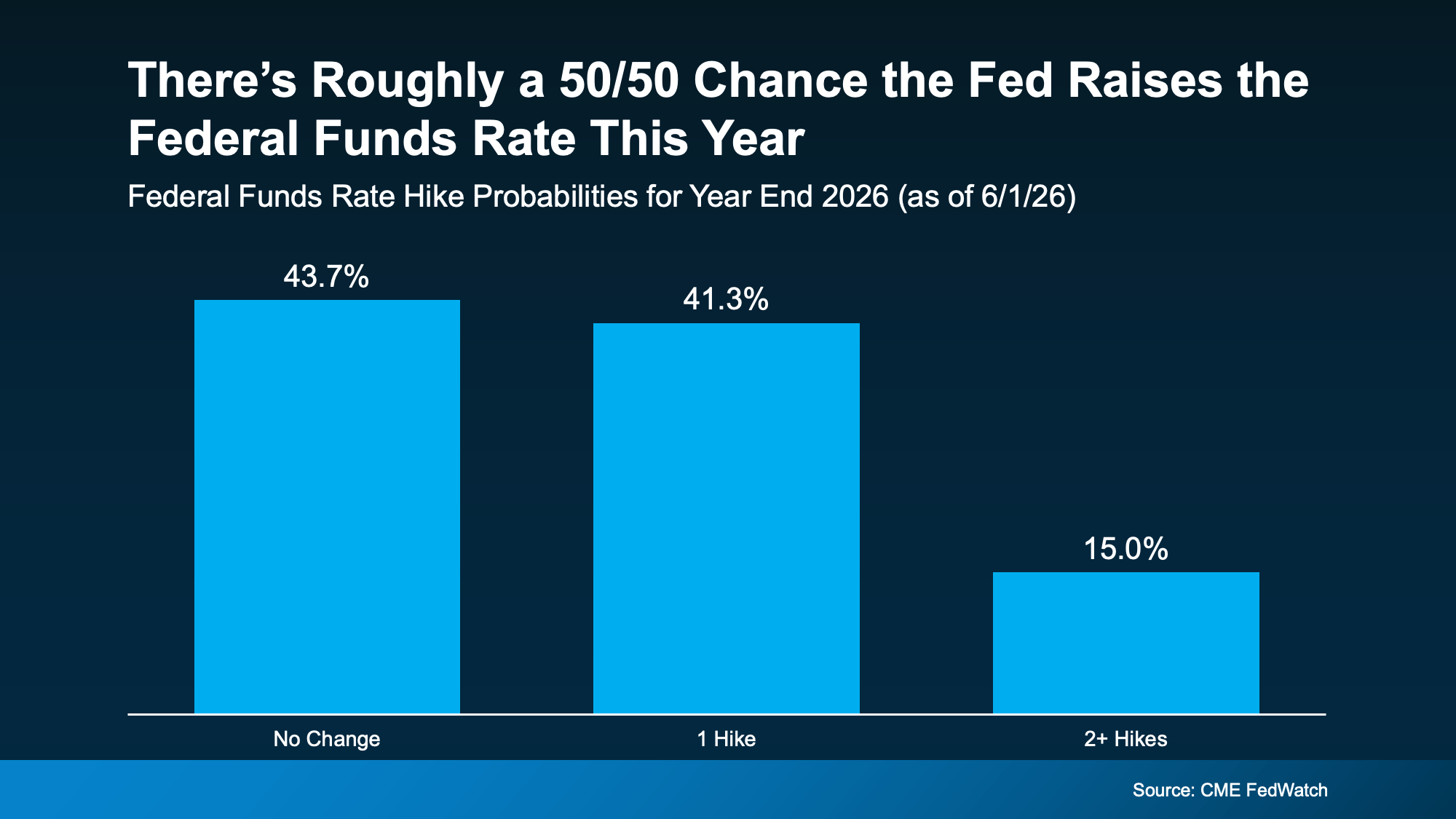

Here’s where this connects to housing. When inflation remains elevated, the Fed is more likely to keep the Federal Funds Rate higher, or potentially raise it, in an effort to slow spending and bring inflation down. While the Federal Funds Rate does not directly determine mortgage rates, it can influence the broader rate environment.

According to CME FedWatch data as of June 2026, market participants were pricing in approximately a 50/50 probability of an additional Federal Funds Rate increase before year end (see graph below):

Source: CME FedWatch, Interest Rate Futures and Options, May 2026. Probabilities reflect market expectations and are not guarantees of future Federal Reserve action.

While it’s too soon to say where this goes for certain and if we’re headed for a rate hike, it does mean mortgage rates are probably not coming down as soon as most people were hoping.

If you've been waiting for rates to drop significantly before making a move, this report is a reminder that "higher for longer" is still very much on the table. It really all depends on where the economy goes from here. According to Bankrate:

“Oil prices and bond yields have dropped a bit . . . but they're still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

Just remember, a tough economy does not equal a housing crash. The conditions today are very different from what led to the 2008 collapse. Here's why:

Uncomfortable and unhealthy are not the same thing. The market feels hard right now, but "hard" and "crashing" are very different.

High rates don't mean homeownership may be out of reach. It just means the path looks a little different. There are real strategies that can help, depending on your situation:

The right strategy, tailored to your goals, matters a lot more than waiting for the perfect moment that may never come.

Inflation is still above where the Fed wants it, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, strategy matters far more than trying to perfectly time the market.

Wondering what this means for your specific situation? Reach out to a First Federal Bank Loan Officer today.

Want to know something important that most people rarely get professionally checked? Spoiler alert: it may be the value of your home.

If you’re planning to buy a home this year, you may be focused on the spring market. And hoping that when spring does hit, you’ll see:

Chances are you’re hearing a lot about mortgage rates right now. You may even see some headlines talking about last week’s Federal Reserve (the Fed)...