Why Owning a Home Is Worth It in the Long Run

Today’s mortgage rates and home prices may have you second-guessing whether it's still a good idea to buy a home right now. While market factors are...

2 min read

Saving for a down payment is often on of the biggest hurdles for prospective homebuyers. With affordability continuing to be a consideration for many households, it's understandable if you've been wondering what it takes to purchase a home in today's market.

One trend worth noting is that many buyers are making purchases with smaller down payments than in recent years.

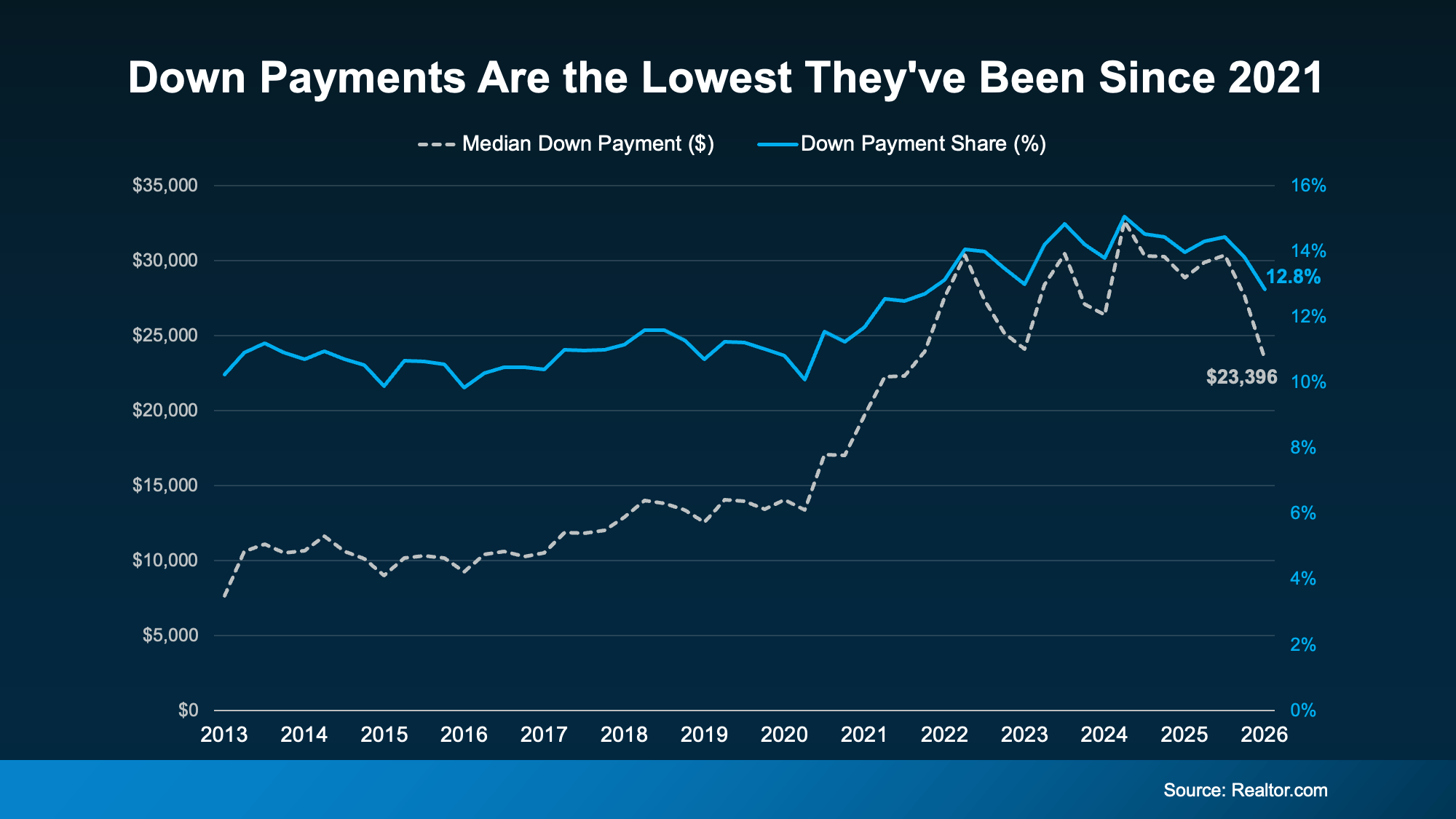

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that's around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

Source: Realtor. com, Down Payments Fall in 2026 as Hosing Market Sags, May 2026. (Data reflects national housing market trends reported by Realtor.com and may not represent conditions in every market or for every borrower).

So why are buyers putting less money down, and how could you potentially put less down, too? Here’s your answer.

There are a few things may be driving the trend:

So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

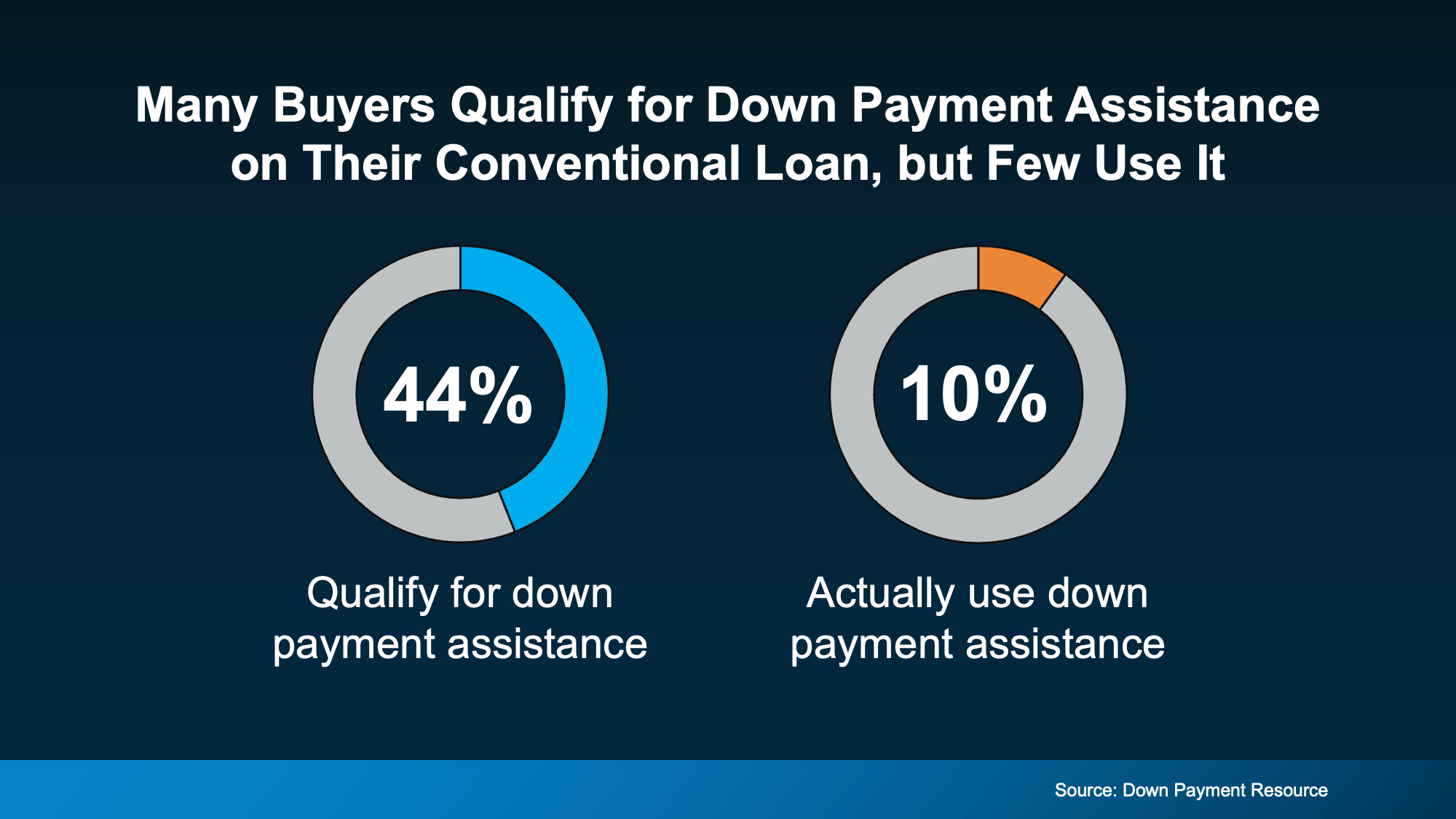

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

Source: Down Payment Resource, Down Payment Assistance Continues to Expand in Q1 2026, April, 2026. (Eligibility for down payment assistance varies by program, income, location, property type, occupancy status, and other factors. Not all applicants will qualify).

The options may be broader than you might assume, too. According to Down Payment Resource (Down payment assistance program availability, funding levels, income limits, property requirements, and other eligibility criteria vary by program and location):

Depending on the loan program, gift funds from eligible family members may also be permitted to help with a down payment or certain closing costs. Documentation requirements and program guidelines apply, and not every loan program allows gift funds in the same way.

If family assistance is being considered, it's important to discuss the details with your lender early in the homebuying process.

Today's housing market looks different than it did just a few years ago, and many buyers are purchasing homes with smaller down payments than in the past. Market conditions, financing options, and assistance programs continue to evolve, making it worthwhile to explore the possibilities that may be available.

If you're considering buying a home, connect with a First Federal Bank Loan Officer to help answer your questions, explain available loan programs, and help you understand your financing options based on your individual circumstances.

Today’s mortgage rates and home prices may have you second-guessing whether it's still a good idea to buy a home right now. While market factors are...

Everyone’s interpretation of the American Dream is unique and personal. But, for many people, it’s tied to a sense of success, freedom, and...