3 min read

Renting can feel much less expensive and much simpler than buying a home, especially right now. No repairs, no property taxes, no worrying about mortgage rates – you just pay the bill and move on with your life.

But here’s the part people don’t talk about enough: renting usually doesn’t help you build equity the way owning can, though everyone’s financial situation is different. Meanwhile, homeowners grow their net worth just by owning a home. Homeowners may build equity over time as they pay down their mortgage and if home values rise – but that depends on the market and individual circumstances.

So, if you’ve been wondering whether buying is still worth it, the long-term math is clearer than you might think.

Renting vs. Owning: How the Costs Really Compare

Let’s break down one of the key differences between renting and buying. When you rent, your payment goes to your landlord, and then it’s gone. When you own, part of your payment comes back to you in the form of equity (the wealth you build as the value of your home increases, and you pay down your home loan).

So, while renting may seem more affordable now, you have to remember it comes at a long-term cost: you’re not building equity in the same way you might with a home, though the right choice really depends on your goals and situation. And it turns out, that’s a bigger miss than you may expect.

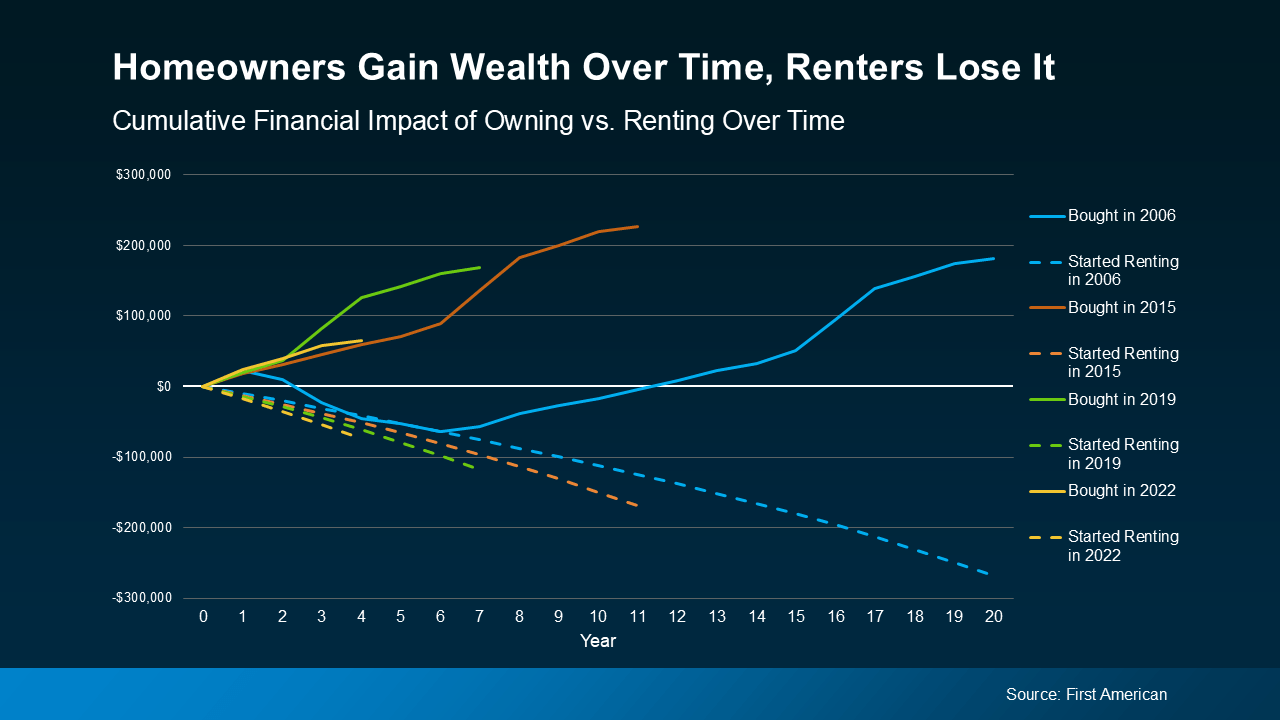

First American recently analyzed the long-term financial impact of renting versus owning a home. They compared mortgage payments, property tax, insurance, repairs, and maintenance against the equity gained through home price appreciation and paying down the mortgage. And they did that during several different time frames to see if it tells a consistent story:

- 2006: the start of the housing bubble

- 2015: 10 years ago

- 2019: just before the pandemic (the last normal years in the market)

- 2022: when mortgage rates jumped

In each time frame, two things were true: renters ended up losing money over time. And homeowners gained it.

Here’s some data so you can see this play out. Each color represents one of the key time frames. The solid lines show the buyer’s investment over time and how their net worth actually grew the longer they lived in their home. The dashed line represents the renter’s investment. In the end, they sank more and more cash into renting without gaining any financial benefit.

Source: Homeownership Remains a Wealth-Generating Engine, First American, August 2025 (This example is meant to show general historical trends and isn’t a guarantee of how things will turn out in the future. Home prices, expenses, and financial outcomes vary from person to person.)

The takeaway is simple: the longer you own your home, the more chances you may have to build equity – while renting doesn’t typically offer that same opportunity. Still, the best choice depends on what works best for you.

Basically, homeowners come out ahead. And the analysis shows that’s even after you factor in the other expenses that come with homeownership, like insurance, repairs, and property taxes. And that's the case for every time frame First American looked into.

On the flip side, renters spent money on their rent, but didn’t gain any long-term financial benefit. That’s true no matter what window of time you look at in the study.

Now, that doesn’t mean buying always beats renting in the short term. But the longer you own, the wider the wealth gap becomes.

Affordability Is Starting To Improve

You might still be thinking, “Okay, but buying feels out of reach for me right now.” Fair.

The past few years haven’t been easy for buyers. But things are starting to shift. Mortgage rates have come down this year, home prices are softening, and incomes have been rising. And according to Zillow, typical monthly payments have gotten a little easier compared to this time last year. Not by a lot, but enough to make a difference.

Bottom Line

Renting may feel less expensive today, but owning is what could build real wealth over time. And with affordability starting to improve, the path to homeownership may be opening up more than you think.

If you’re curious what buying could look like for you, you can always connect with a First Federal Bank Loan Officer to explore what your options might look like, based on your situation.

The content on this site is intended for informational purposes only and should not be considered accounting, legal, real estate, tax, or financial advice. First Federal Bank recommends that customers conduct their own research and consult with professional legal and financial advisors before making any financial decisions. Links to third-party websites may be provided for your convenience; however, First Federal Bank does not guarantee the reliability, accuracy, or safety of the information, products, or services offered on these external sites. We are not liable for any damages resulting from the use of these links, and we do not investigate, verify, or endorse the content or opinions expressed on any third-party sites. First Federal Bank | Equal Housing Lender | NMLS # 408902

Don’t Miss Out on the Growing Number of Down Payment Assistance Programs

With rising home prices and volatile mortgage rates, it’s important you know about every resource that could help make buying a home possible. And...

Buying a Home May Help Shield You from Inflation

It feels like everything is getting more expensive these days. That’s because inflation has remained higher than normal for longer than expected –...