2 min read

If you've been following the headlines, it's easy to assume the housing market is struggling. While affordability and interest rates remain important factors for many buyers, the overall market tells a more balanced story.

The housing market today looks very different than it did during 2020 and 2021. Those years were marked by historically low mortgage rates, limited inventory, and exceptionally high buyer demand. Based on available market data, today's market reflects a return toward more typical conditions.

Many Homeowners may have built significant equity.

Many homeowners may have accumulated substantial equity over the past several years through home appreciation and paying down their mortgage balances. According to available housing data, homeowner equity has remained at historically high levels nationwide.

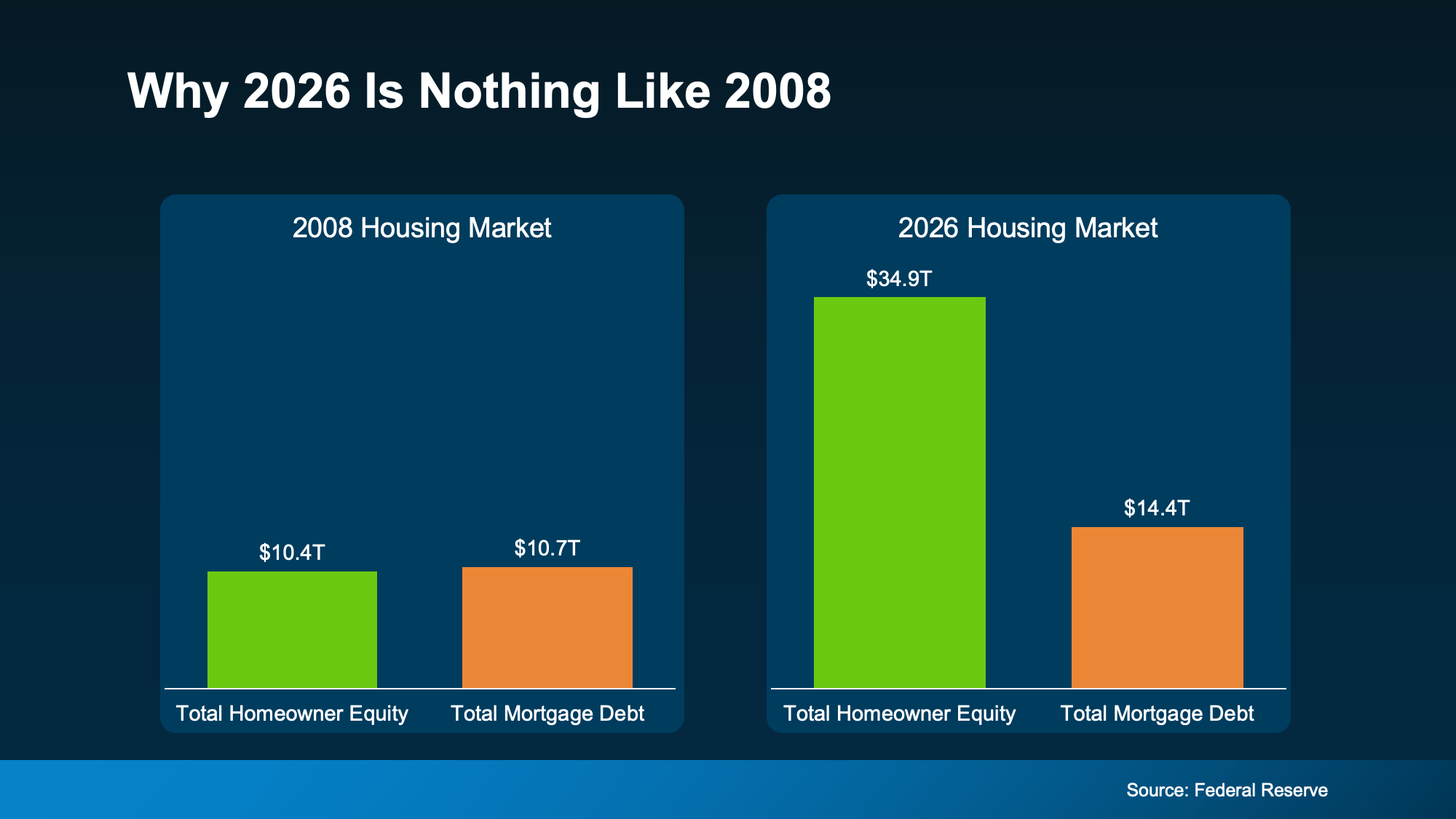

Today? Total homeowner equity across the country sits at $35 trillion – dwarfing total mortgage debt (see graph below):

Source: Federal Reserve Bank, Households; Owners Equity in Real Estate, June 2026

That gap may indicate that many homeowners have accumulated meaningful equity, which may provide additional financial flexibility depending on their individual circumstances. If they needed to sell, many may be better positioned to do so because of that equity.

- Realtor.com found that homeowners who've been in their home just 5 years have built up around $180,000 in equity on average. Stick around 6-10 years, and that jumps to over $340,000.

- Data from ATTOM and the Census shows two-thirds of homeowners either own their home outright or have more than 50% equity.

That's not a fragile market. That’s a population of homeowners who may be financially positioned to sell, to stay, or to make their next move from a place of strength rather than pressure.

Low Rates and Low Foreclosures

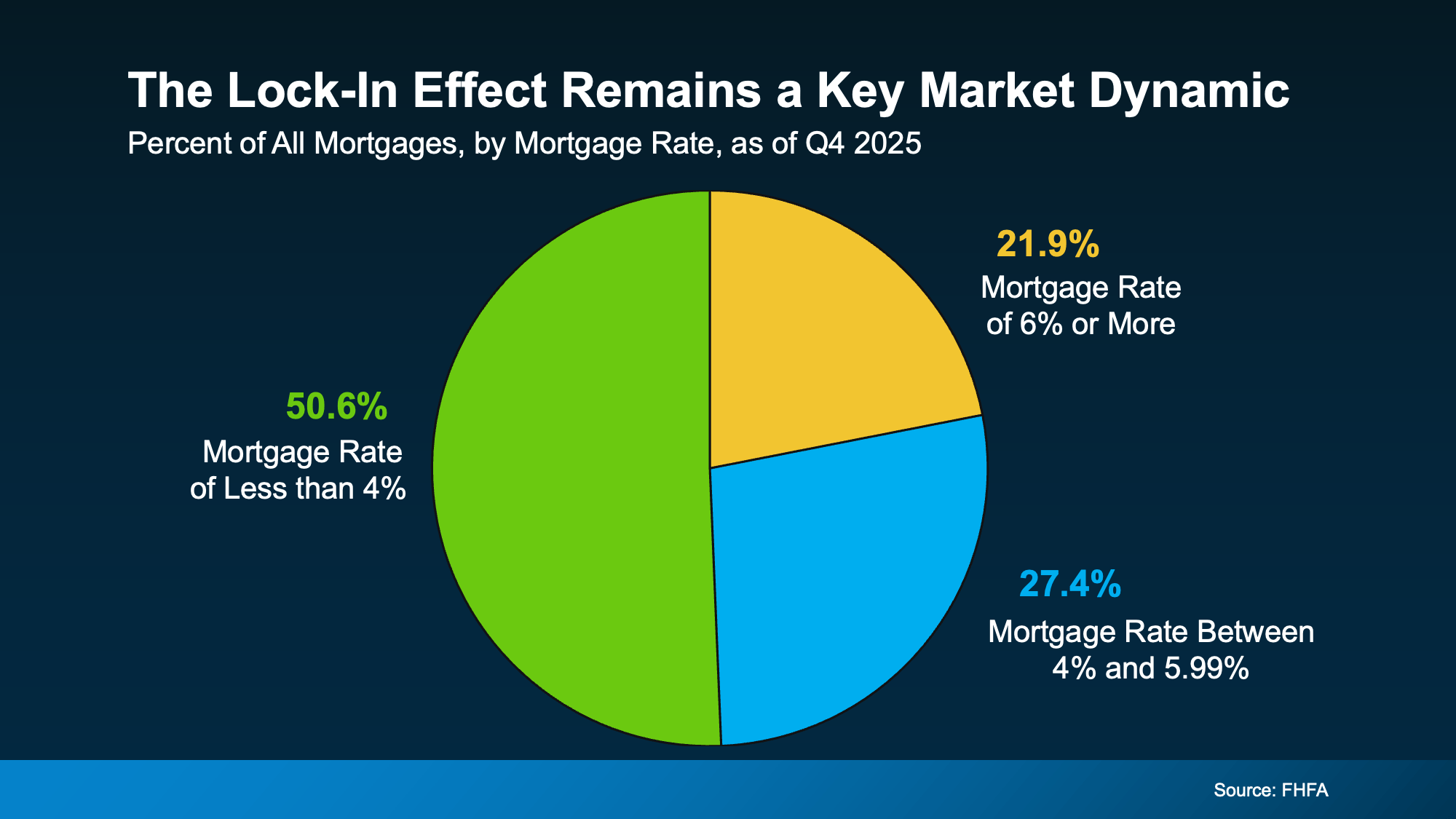

At the same time, Federal Housing Finance Agency (FHFA) data shows more than half of all active mortgages still carry a rate below 4% (see graph below). These figures reflect the overall mortgage market and are not rates offered by First Federal Bank.

Source: FHFA, National Mortgage Database Aggregate Statistics, January 2026

That's a big reason inventory stays tight. Those homeowners aren't in a rush to trade their rate for a higher one. Many homeowners continue to benefit from lower mortgage rates and accumulated equity, although individual financial circumstances vary.

That comfort shows up in the foreclosure numbers, too. Despite a slight recent uptick, foreclosure volumes remain dramatically below historical norms, according to ATTOM. Some homeowners have equity, they have breathing room, and most have options that keep them out of financial distress.

Prices Are Showing Signs Stabilizing, Not Crashing

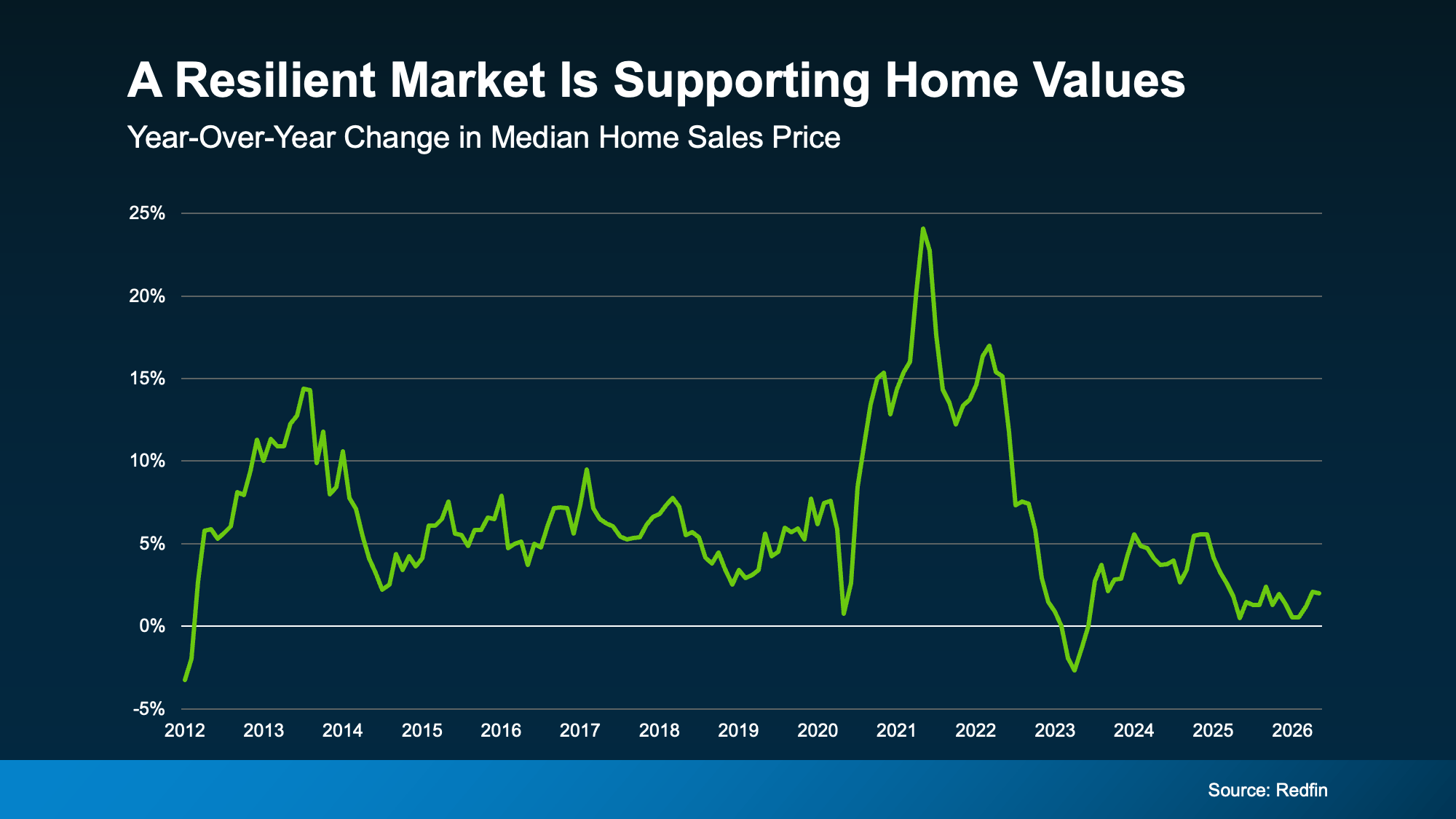

Here’s another point on the resilience of the market. Redfin research shows home prices are still rising, but the pace has slowed, now closer to 2% year-over-year nationally (see graph below):

Source: Redfin, United States Housing Market, May 2026

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

“We’re in the middle of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy sent prices soaring and inventory to historic lows, the market needed a reset.”

Bottom Line

Real estate conditions can vary significantly by community, price range, and individual circumstances. Whether you're considering buying, selling, refinancing, or simply gathering information, it's important to understand how current market conditions apply to your specific situation.

If you have questions about today's mortgage options or would like to review your financing choices, connect with a First Federal Bank Loan Officer, to discuss the financing options that may be available based on your individual circumstances.

The content on this site is intended for informational purposes only and should not be considered accounting, legal, real estate, tax, or financial advice. First Federal Bank recommends that customers conduct their own research and consult with professional legal and financial advisors before making any financial decisions. Links to third-party websites may be provided for your convenience; however, First Federal Bank does not guarantee the reliability, accuracy, or safety of the information, products, or services offered on these external sites. We are not liable for any damages resulting from the use of these links, and we do not investigate, verify, or endorse the content or opinions expressed on any third-party sites. First Federal Bank | Equal Housing Lender | NMLS # 408902

Homebuyers Are Still Active: What Today's Market May Mean for You

If you've been thinking about selling, you've probably seen plenty of headlines suggesting the real estate market has slowed significantly. While...